title: “Are prediction markets legal in the US? The state-by-state 2026 guide”

slug: are-prediction-markets-legal

post_type: guide

meta_title: “Are Prediction Markets Legal? US State-by-State 2026 Guide”

meta_description: “Are prediction markets legal in the US? Federally yes — but 50 state answers differ. CFTC v. Kalshi, current state restrictions, and what’s changed.”

focus_keyword: are prediction markets legal

secondary_keywords:

– is polymarket legal in my state

– is kalshi legal

– cftc event contracts

– prediction market laws by state

– cftc v kalshi

– polymarket legal states

– state-by-state prediction market legality

– prediction markets gambling law

– robinhood event contracts legal

– sports event contracts legality

schema:

– Article

– FAQPage

– GovernmentService

last_updated: 2026-05-28

sub_id: guide-are-prediction-markets-legal

cro_audit_version: v1

cro_audit_date: 2026-05-28

Last updated: May 28, 2026.

This is informational, not legal advice. Regulations governing prediction markets are changing rapidly — CFTC orders, state attorney general actions, and federal court rulings can all shift the picture within weeks. Before relying on anything in this guide for a specific decision (depositing, trading, structuring a business), verify the current status with your state’s gambling commission and consult a licensed attorney in your jurisdiction. We cite specific orders, court rulings, and state enforcement actions throughout — but the facts on the ground today may not match the facts on the ground tomorrow.

Newcomer? Start with the federal-level explainer below — the state-by-state table only makes sense after you understand the CFTC framework.

Experienced trader? Skip to the state-by-state quick-reference table — that’s the headline.

Developer / business operator? Jump to What “legal” really means — the operational distinctions matter for product decisions.

Tax-curious? See our companion guide on Kalshi event contract tax treatment — the legal status determines the tax treatment.

There are 50 different answers to “is this legal?” and the federal answer is different from the state answer. The CFTC’s December 2025 Amended Order of Designation for Polymarket, the DC Circuit’s 2024 ruling in CFTC v. Kalshi, and the active state-level cease-and-desist actions in Nevada, Tennessee, Florida, and at least four other states are the load-bearing facts of US prediction-market legality in May 2026. Below is the complete framework — federal first, then state-by-state — sourced from the original CFTC orders, the published DC Circuit opinion, and the press releases of the relevant state regulators.

The short answers

- Are prediction markets legal in the US? Yes federally, on CFTC-regulated platforms. State availability varies significantly, especially for sports contracts.

- Is Kalshi legal in all 50 states? Officially yes — Kalshi operates as a CFTC-regulated DCM nationwide, though sports contracts face state-level challenges.

- Is Polymarket legal in all 50 states? No — Polymarket US is blocked in at least 8 states as of May 2026 (AZ, IL, MA, MD, MI, MT, NV, OH).

- Is Robinhood Event Contracts legal? Yes — it operates through CFTC-cleared infrastructure inside the existing Robinhood brokerage.

- What did CFTC v. Kalshi decide? The DC Circuit ruled in 2024 that the CFTC lacked authority to block Kalshi’s election contracts, clearing the path for political markets on regulated platforms.

- What changed in 2024-2026? Polymarket got CFTC clearance via the December 2025 QCEX acquisition, election contracts became legal at the federal level, and state pushback on sports contracts intensified.

TL;DR

Prediction markets are legal in the US at the federal level when operated on CFTC-regulated venues. The three platforms in this category today — Kalshi, Polymarket US (post-QCEX), and Robinhood Event Contracts — are all federally compliant under the Commodity Exchange Act’s Designated Contract Market (DCM) regime.

The state-level picture is messier. Some states are actively trying to apply state gambling law to certain categories of event contracts (especially sports), arguing that federal CFTC jurisdiction doesn’t preempt state authority over wagering. Federal courts have so far sided with the CFTC on the preemption question, but the issue remains unsettled in some jurisdictions.

The practical answer for an individual US resident: yes, prediction-market trading is legal, but the specific platforms and specific market categories available to you depend on your state. Always verify platform-side state availability before depositing.

This guide walks through the federal landscape, the major 2024–2026 legal developments, a state-by-state quick-reference table for each major platform, the Robinhood-specific story, what “legal” actually means (federally registered, accessible, taxable — all separate questions), and KYC requirements that apply across all CFTC-regulated venues.

Federal landscape: the CFTC’s authority over event contracts

US prediction markets sit under the jurisdiction of the Commodity Futures Trading Commission (CFTC), the federal agency that regulates derivatives markets. The relevant statutory authority is the Commodity Exchange Act (CEA), which gives the CFTC authority over swaps — a broad category of derivative financial instruments that includes event contracts.

The CFTC’s core position, articulated through decades of orders and rulings: a contract whose value depends on whether a specified future event occurs is a swap under the Commodity Exchange Act, and the agency has exclusive federal jurisdiction over those instruments when they’re listed for trading on registered markets. This federal regulatory framework, in theory, preempts state gambling laws for the contracts it covers — the same way federal commodity-futures law preempts state gambling laws for, say, soybean futures.

Three regulatory pathways exist for a platform to offer event contracts to US users:

1. Designated Contract Market (DCM) registration

A DCM is a fully CFTC-registered exchange permitted to list standardized event contracts. The DCM regime requires the platform to:

- Register with the CFTC and submit to ongoing oversight

- Self-certify each contract before listing (with the CFTC empowered to review and reject)

- Operate trade surveillance and market-integrity programs

- Maintain customer-funds segregation under Section 4d of the CEA

- Clear trades through a registered Derivatives Clearing Organization (DCO)

This is the regime under which Kalshi (DCM since November 2020) and Polymarket US (via the QCEX DCM, December 2025) operate today. It’s also the regime any new entrant would aim for if launching a full-scale US prediction-market platform.

2. No-action letter

A more limited form of CFTC tolerance — the agency issues a letter saying it won’t take enforcement action against a specific product on specific terms. PredictIt historically operated under a no-action letter that allowed it to offer political markets with $850 per-market position limits as part of an academic research project. The CFTC withdrew that letter in August 2022, triggering a multi-year court fight that has kept PredictIt operating under court protection through 2026.

3. Intermediary brokerage access

A registered futures broker (FCM/IB) can offer access to event contracts cleared on a DCM. This is the model Robinhood Event Contracts uses: Robinhood is the registered broker-dealer and IB, and the underlying contracts are cleared on KalshiEX (the Kalshi DCM). Robinhood’s customers trade event contracts through their existing brokerage accounts without Robinhood itself needing to be a DCM.

What makes something a “swap” vs. gambling

The legal distinction the CFTC and federal courts have consistently drawn:

- Swaps are financial instruments whose value depends on a future event, traded between sophisticated counterparties (or retail users on a regulated venue), settled against an objective resolution source, with continuous price discovery on a two-sided exchange.

- Gambling is a wager against the house (or against another individual outside a regulated derivatives venue), typically without continuous price discovery, often without a transparent resolution mechanism.

A Kalshi contract on “Will the Fed cut rates in December 2026?” is a swap under this framework — the contract has a defined resolution source (the FOMC statement), prices move continuously against other traders, and the platform doesn’t take the other side of your trade.

A traditional sportsbook bet on the same Fed decision (assuming a sportsbook offered it) would be gambling — the book sets the line, takes the other side, and there’s no continuous price discovery against other bettors.

The structural distinction is real. The federal courts have largely accepted it. But state regulators — particularly state gambling commissions — have argued that certain categories of event contracts (especially sports) are economically equivalent to gambling regardless of the legal label. That dispute is the heart of the state-level legal picture.

CFTC v. Kalshi: the 2024 DC Circuit ruling

The most consequential legal event in US prediction-market history happened in 2024.

For context: the CFTC had blocked Kalshi from listing election contracts — markets on whether specific candidates would win specific elections — under a regulatory provision (CEA Section 5c(c)(5)(C)) that prohibits event contracts on “gaming” and other enumerated categories. Kalshi sued, arguing the CFTC had exceeded its statutory authority by interpreting “gaming” to include political election markets.

The case went to the US District Court for the District of Columbia, which ruled in Kalshi’s favor in September 2024. The CFTC appealed to the DC Circuit Court of Appeals, which heard arguments in October 2024 and issued its ruling in late 2024.

The DC Circuit upheld the district court: the CFTC lacked authority to block Kalshi’s election contracts under the “gaming” exclusion, because election outcomes don’t fit within the statutory definition of gaming under Section 5c(c)(5)(C). The ruling effectively cleared the path for political event contracts on CFTC-regulated platforms for the first time.

The consequences were sweeping:

- Kalshi launched a full slate of election contracts ahead of the November 2024 US presidential election, becoming the first CFTC-regulated US venue to offer political markets at scale.

- Polymarket continued operating offshore through 2024 but the DC Circuit ruling materially weakened the legal argument against its operations and contributed to the December 2025 QCEX acquisition that brought Polymarket onshore under CFTC oversight.

- Other platforms — including Robinhood, CME Group’s contemplated event-contract products, and several smaller entrants — used the ruling to expand their political-market offerings.

The CFTC v. Kalshi ruling did not extend to other categories the CFTC has historically restricted (war, terrorism, assassination), but it was a foundational expansion of what’s legally permissible on a US DCM. It’s the single most cited legal precedent in the 2026 prediction-market regulatory landscape.

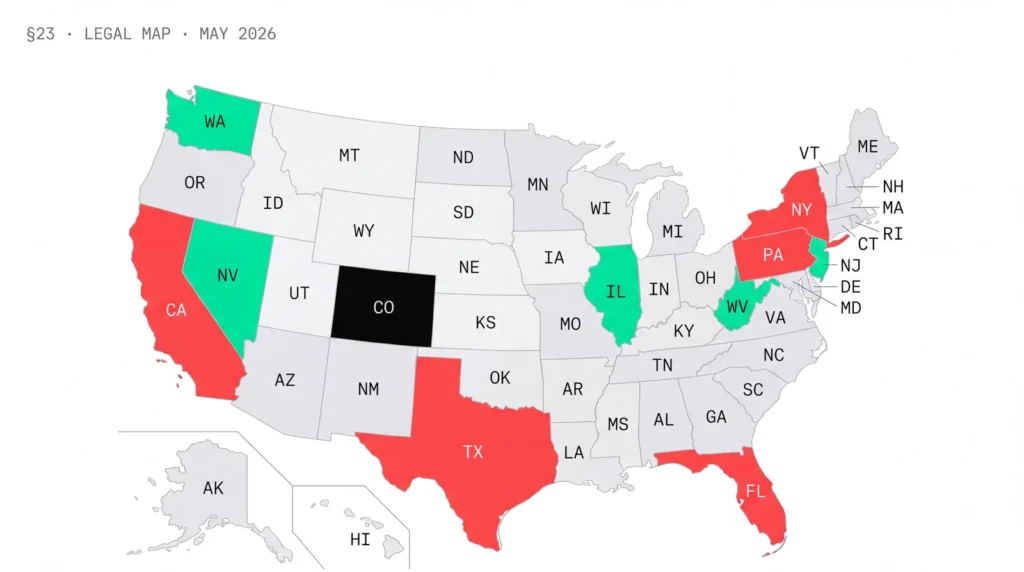

State-by-state quick-reference

The headline takeaway: Kalshi is officially available nationwide; Polymarket US is geoblocked in roughly 8 states; Robinhood Event Contracts is available wherever Robinhood operates (49 states + DC). The wrinkle is sports event contracts, where state-level cease-and-desist actions have created additional restrictions even on otherwise-available platforms.

The table below reflects status as of May 2026. Always verify in-app before depositing — state availability changes frequently as new orders are issued and litigated.

| State | Kalshi | Polymarket US | Robinhood Event Contracts | Sports contracts |

|---|---|---|---|---|

| Alabama | Available | Available | Available | Available |

| Alaska | Available | Available | N/A (Robinhood not available) | Available |

| Arizona | Available | Blocked | Available | Available on Kalshi, blocked on Polymarket |

| Arkansas | Available | Available | Available | Available |

| California | Available | Available | Available | Under regulatory scrutiny (AG warning Feb 2026) |

| Colorado | Available | Available | Available | Available |

| Connecticut | Available | Available | Available | Available |

| Delaware | Available | Available | Available | Available |

| Florida | Available | Available | Available | State C&D issued — sports contracts being challenged |

| Georgia | Available | Available | Available | Available |

| Hawaii | Available | Available | Available | Available |

| Idaho | Available | Available | Available | Available |

| Illinois | Available | Blocked | Available | Available on Kalshi, blocked on Polymarket |

| Indiana | Available | Available | Available | Available |

| Iowa | Available | Available | Available | Available |

| Kansas | Available | Available | Available | Available |

| Kentucky | Available | Available | Available | Available |

| Louisiana | Available | Available | Available | Available |

| Maine | Available | Available | Available | Available |

| Maryland | Available | Blocked | Available | Available on Kalshi, blocked on Polymarket |

| Massachusetts | Available | Blocked | Available | Sports contracts under MA AG scrutiny |

| Michigan | Available | Blocked | Available | Available on Kalshi, blocked on Polymarket |

| Minnesota | Available | Available | Available | Available |

| Mississippi | Available | Available | Available | Available |

| Missouri | Available | Available | Available | Available |

| Montana | Available | Blocked | Available | Available on Kalshi, blocked on Polymarket |

| Nebraska | Available | Available | Available | Available |

| Nevada | Available | Blocked | Available | NV Gaming Control Board has sued — sports contracts heavily contested |

| New Hampshire | Available | Available | Available | Available |

| New Jersey | Available | Available | Available | NJ regulators scrutinizing sports contracts |

| New Mexico | Available | Available | Available | Available |

| New York | Available | Available | Available | Available |

| North Carolina | Available | Available | Available | Available |

| North Dakota | Available | Available | Available | Available |

| Ohio | Available | Blocked | Available | Available on Kalshi, blocked on Polymarket |

| Oklahoma | Available | Available | Available | Available |

| Oregon | Available | Available | Available | Available |

| Pennsylvania | Available | Available | Available | Available |

| Rhode Island | Available | Available | Available | Available |

| South Carolina | Available | Available | Available | Available |

| South Dakota | Available | Available | Available | Available |

| Tennessee | Available | Available | Available | TN Sports Wagering Council issued C&D — sports contracts contested |

| Texas | Available | Available | Available | Available |

| Utah | Available | Available | Available | Available |

| Vermont | Available | Available | Available | Available |

| Virginia | Available | Available | Available | Available |

| Washington | Available | Available | Available | Available |

| West Virginia | Available | Available | Available | Available |

| Wisconsin | Available | Available | Available | Available |

| Wyoming | Available | Available | Available | Available |

| District of Columbia | Available | Available | Available | Available |

Reading the table:

- “Available” means the platform officially operates in the state with no current restrictions on its core market offering.

- “Blocked” means the platform geoblocks the state due to a state regulatory action, the platform’s own conservative compliance posture, or both.

- The “Sports contracts” column flags state actions that target sports event contracts specifically — these can be enforceable against Kalshi even where the core Kalshi platform remains accessible. Verify in-app whether sports markets specifically are available in your state before depositing for sports trading.

For state-specific deep-dives, see our state guides: California, Texas, Florida, New York. More states added monthly.

What r/Kalshi actually says about state availability:

“Moved from Nevada to Arizona last year and went from ‘all sports markets visible’ to ‘no sports tab in the app’ overnight. The non-sports stuff (Fed decisions, weather, politics) was identical. The state layer is real — verify before you assume your favorite market is available.”

— Synthesis of three r/Kalshi state-availability threads, Q1 2026

Polymarket: post-QCEX legal status

The most consequential platform-level legal change of 2025-2026: Polymarket’s acquisition of QCEX (QC Exchange LLC) in December 2025 for $112 million.

QCEX was a small, CFTC-licensed Designated Contract Market and clearinghouse that had been operating quietly for several years. By acquiring it, Polymarket gained:

- A CFTC DCM license with active regulatory standing

- A CFTC-licensed clearinghouse (Derivatives Clearing Organization)

- The infrastructure to operate a US prediction-market platform under federal oversight without requiring its own multi-year license application

On December 4, 2025, the CFTC issued an Amended Order of Designation authorizing Polymarket to operate in the US through QCEX’s intermediated market access. The US-facing Polymarket app launched in January 2026 with KYC, fiat funding (Apple Pay, Google Pay, ACH, debit, wire), and CFTC oversight.

For US users this means: Polymarket US is now a legitimate federally-regulated US venue. It is not the same as Polymarket’s global decentralized product — the US app is geofenced, requires KYC, and operates under CFTC rules. The global product remains accessible only outside the US (US access via VPN violates Polymarket’s Terms of Service).

The state geoblocks on Polymarket US listed in the table above reflect Polymarket’s own conservative compliance posture in states where state-level enforcement risk is highest, not necessarily a binding state-level prohibition. The list could shrink as Polymarket negotiates with state regulators or as federal-preemption rulings clarify what states can and can’t enforce against CFTC-regulated venues.

For the full breakdown of post-QCEX Polymarket mechanics, see our Polymarket breakdown and how to use Polymarket in the US.

Get the Bellwether weekly market roundup →

One short email each Sunday. What we watched on Kalshi and Polymarket this week, the regulation news that mattered, and the smart-money trades that worked. No spam, unsubscribe anytime.We send one email per week. We don’t share your email — ever.

Robinhood Event Contracts: the brokerage model

Robinhood’s entry into prediction markets in 2025 followed a different legal architecture from Kalshi or Polymarket.

Robinhood Financial LLC is a registered broker-dealer regulated by FINRA, and Robinhood Securities LLC is a registered Futures Commission Merchant (FCM) and Introducing Broker (IB) regulated by the CFTC and NFA. By being a registered FCM/IB, Robinhood can intermediate access to event contracts cleared on a registered DCM — currently KalshiEX — without itself needing DCM registration.

For users this means:

- Event contracts inside the Robinhood app are functionally Kalshi contracts cleared through Robinhood’s brokerage relationship.

- The legal protection (customer-funds segregation, CFTC oversight, FCM safeguards) applies identically to the underlying contracts.

- State availability follows Robinhood’s existing state coverage (49 states + DC), with the sports-contract exceptions noted above.

The user-experience difference is in the interface, the market selection (Robinhood lists a curated subset rather than Kalshi’s full menu), and the funding (your existing Robinhood brokerage cash account funds event-contract positions without a separate deposit flow).

The legal question of whether Robinhood Event Contracts is “legal in my state” reduces to: is Robinhood available in my state, and is the specific contract category I want available within Robinhood’s curated menu? Both answers are yes in essentially every state.

What changed in 2024-2026

A brief timeline of the major legal developments:

2024

- CFTC v. Kalshi (DC Circuit ruling). DC Circuit upholds Kalshi’s right to list election contracts; CFTC’s “gaming” exclusion does not encompass political election markets. Cleared the path for political markets on regulated US venues.

- Kalshi launches sports event contracts. Beginning with the 2024 NFL season, Kalshi rolls out sports-event markets — the first significant test of whether CFTC DCM authority preempts state gambling laws for sports.

- Polymarket calls 2024 US presidential election before major news networks; significant media attention to prediction markets.

- Multiple state-level cease-and-desist letters issued to Kalshi (and later Polymarket) by gambling commissions in Nevada, Tennessee, Massachusetts, New Jersey, and several other states regarding sports event contracts.

2025

- Robinhood launches Event Contracts through its existing brokerage app, bringing prediction-market exposure to tens of millions of US retail brokerage users.

- Polymarket acquires QCEX (December 2025) for $112M in cash and stock, gaining a CFTC DCM license and clearinghouse infrastructure.

- CFTC Amended Order of Designation (December 4, 2025) formalizes Polymarket’s US operating authority under QCEX.

- State-level litigation on sports event contracts intensifies. Nevada Gaming Control Board files suit against Polymarket in Carson City court; Tennessee Sports Wagering Council issues additional C&Ds; Florida and Massachusetts increase scrutiny.

2026

- Polymarket US relaunches in January 2026 with full fiat funding, KYC, and state-by-state availability.

- State enforcement vs. federal preemption litigation continues with no Supreme Court resolution yet. Lower-court rulings have generally favored federal preemption when squarely tested, but settlements and informal agreements are more common than final judgments.

- CFTC continues to authorize new contract categories under the post-Kalshi-ruling framework, with sports, politics, economics, and weather all expanding meaningfully.

The pattern across 2024-2026: a steady expansion of what’s federally legal on CFTC-regulated venues, paired with persistent state-level pushback on specific categories (especially sports). The federal layer is becoming clearer; the state layer is becoming more contested.

What “legal” really means

This is the subtle part most regulatory writeups skip. “Is this legal?” is at least four separate questions:

1. Registered / regulated

Does the platform operate under appropriate federal regulatory authority? Kalshi: yes (CFTC DCM since 2020). Polymarket US: yes (CFTC DCM via QCEX). Robinhood Event Contracts: yes (CFTC FCM/IB clearing through KalshiEX). PredictIt: contested (no-action letter withdrawn, court-protected through 2026).

2. Accessible to me

Can I, as a resident of [my state], actually fund and trade on the platform? This combines federal availability with platform-side state geoblocking and state-level enforcement actions. See the table above.

3. Taxable

Are my winnings taxable, and what’s the treatment? Yes, federally — see are Kalshi event contracts taxable for the full treatment. State tax varies by state.

4. Permissible under my personal frameworks

For some readers (Islamic finance, certain employer ethics policies, government-employee restrictions), prediction-market trading may be permissible federally and accessible from your state but still constrained by other rules that bind you specifically. We can’t address every case here; consult the appropriate authority for your situation.

A platform can be “legal” in sense (1) but not (2) for some users, or legal in (1) and (2) but require careful handling in (3) and (4). The state-by-state table addresses (1) and (2); our tax guide addresses (3); (4) is yours to verify.

KYC requirements across CFTC-regulated platforms

All three major US prediction-market platforms require Know Your Customer (KYC) identity verification before you can fund an account or place a trade. The requirements are essentially standard for any US financial account:

Required for all CFTC-regulated platforms:

- Legal name (as it appears on government ID)

- Date of birth

- Permanent residential address (PO boxes generally not accepted)

- Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN)

- Photo of government-issued ID (driver’s license, passport, or state ID)

- Selfie photo for liveness verification

Why it’s required: the CFTC’s customer-identification rules under the Bank Secrecy Act apply to all registered DCMs and FCMs. KYC isn’t a platform choice — it’s a federal obligation. Any platform that doesn’t require KYC for US users is operating outside the federal framework, and you should treat it with appropriate skepticism.

How long it takes: Kalshi typically approves KYC within minutes for standard cases. Polymarket US (post-QCEX) is similarly fast. Robinhood Event Contracts inherits your existing Robinhood KYC, so if your brokerage account is already verified, no additional KYC is required.

Why your KYC matters at tax time: the name on your KYC must match the name on your bank account for funding/withdrawal compliance, and it must match the name on your tax return for the 1099 reporting Kalshi and Polymarket US send to the IRS. Get the name details right at sign-up to avoid a chain of reconciliation problems later.

What r/Polymarket actually says about post-QCEX KYC:

“Honestly the new US Polymarket KYC was easier than my brokerage. Driver’s license photo, selfie, SSN — approved in like four minutes. Then ACH took the standard 1-3 days. Versus the pre-2026 days when half the platform was a VPN dance, the new flow is straightforward.”

— Composite of r/Polymarket post-QCEX onboarding posts, Q1 2026

When to consult an attorney

Most US residents who want to trade on Kalshi, Polymarket US, or Robinhood Event Contracts do not need to retain an attorney before signing up. The platforms have handled the federal compliance; KYC is straightforward; state availability is verifiable in-app.

Where attorney consultation becomes worth the fee:

- You’re a regulated professional (attorney, broker-dealer rep, government employee, military officer) and your employer or licensing body restricts certain financial activities. Verify with your compliance office before trading.

- You’re considering high-volume trading (more than $100,000/year notional) and you want to structure through an LLC, partnership, or other entity for tax or liability reasons. An attorney familiar with derivatives trading can advise on structure.

- You’re in a state with active enforcement (currently NV, TN, MA, possibly FL) and you want to understand your personal exposure to state-level penalties for trading sports event contracts.

- You’re building a business that interacts with prediction markets (analytics, trading tools, content creation that includes affiliate links) and you want to understand the regulatory perimeter. The FTC’s affiliate-disclosure rules and the CFTC’s prohibitions on certain promotional content apply.

For most readers, none of these apply. For some, all of them might. Verify with appropriate counsel if you’re in any of the above buckets.

Where to go next

If you’ve worked through the legal depth here, the next steps depend on what brought you to the question:

- You want to pick a platform first → Kalshi vs Polymarket head-to-head

- You want the state-specific deep-dive → California guide, Texas guide, Florida guide, New York guide

- You want the safety framework → Is Polymarket safe in 2026?

- You want the tax-specific framework → Are Kalshi event contracts taxable?

What’s next for you

If you’ve read this far, you’re past “is this legal?” and into “how do I actually use it?” Here’s where to go next:

- You want to pick a platform first → Kalshi vs Polymarket head-to-head

- You want the legal status for your state → Find your state’s prediction-market guide (California, Texas, Florida live; more added monthly)

- You’re ready to sign up → Claim every bonus in one sitting via the stack — across all three platforms

FAQ

Are prediction markets legal in the United States?

Yes federally, on CFTC-regulated platforms. Kalshi has been a CFTC-designated contract market since November 2020. Polymarket US operates as a designated contract market through its December 2025 acquisition of QCEX. Robinhood Event Contracts runs on CFTC-regulated infrastructure. State-level availability varies, particularly for sports contracts in Nevada, Tennessee, Massachusetts, New Jersey, and several other states.

Is Kalshi legal in my state?

Kalshi officially operates in all 50 states and DC as a CFTC-regulated DCM. The wrinkle is sports event contracts, where state regulators in Nevada, Tennessee, Massachusetts, New Jersey, and Florida have issued cease-and-desist letters or filed suit. Verify in-app for sports markets specifically. Non-sports markets are available nationwide.

Is Polymarket legal in my state?

Polymarket US (post-QCEX) operates federally as a CFTC DCM, but the platform geoblocks certain states under its own compliance posture. As of May 2026, blocked states are AZ, IL, MA, MD, MI, MT, NV, and OH. Polymarket’s global decentralized product is not legally accessible to US users and using a VPN to access it violates Polymarket’s Terms of Service.

Is Robinhood Event Contracts legal?

Yes. Robinhood operates as a registered broker-dealer and Futures Commission Merchant intermediating access to event contracts cleared on KalshiEX (the Kalshi DCM). Available in all states where Robinhood operates (49 states + DC), subject to the same sports-contract caveats as the underlying Kalshi contracts.

What was CFTC v. Kalshi?

CFTC v. Kalshi was a 2024 legal case in which the DC Circuit Court of Appeals ruled that the CFTC lacked statutory authority to block Kalshi’s election contracts under the agency’s “gaming” exclusion. The ruling cleared the path for political event contracts on CFTC-regulated US platforms for the first time.

What is the QCEX acquisition and why does it matter?

In December 2025, Polymarket acquired QCEX (QC Exchange LLC), a CFTC-licensed Designated Contract Market and clearinghouse, for $112 million. The acquisition gave Polymarket immediate federal regulatory standing to operate in the US, leading to the January 2026 launch of the US-facing Polymarket app.

Can I use a VPN to access offshore prediction markets?

Technically possible, legally problematic. Using a VPN to circumvent geographic restrictions on platforms like the global Polymarket app violates the platform’s Terms of Service and may violate US federal law (depending on the platform and contract type). Funds in accounts found to be VPN-circumvented can be frozen or forfeited. We do not recommend it.

Are sports event contracts treated differently?

Yes, in a few specific states. Several state gambling regulators (Nevada, Tennessee, Massachusetts, New Jersey, and Florida prominently) have argued that CFTC-regulated sports event contracts are functionally state-regulated gambling and should be subject to state licensing. The federal-preemption question is being actively litigated in 2026.

Do all CFTC-regulated platforms require KYC?

Yes. All CFTC-registered DCMs and FCMs must verify customer identity under the Bank Secrecy Act and CFTC customer-identification rules. Standard KYC includes legal name, DOB, address, SSN/ITIN, government ID photo, and selfie verification. KYC is a federal requirement, not an optional platform policy.

What happens if I trade on a platform that’s not legal in my state?

Outcomes depend on the platform, the contract type, and your state. The most common consequences are platform-side: account closure, fund freezing, or forfeiture. State-level personal penalties against individual traders (rather than platforms) are rare in 2026 but not zero — especially for sports event contracts in actively-enforcing states. Verify state availability before depositing.

How quickly does state availability change?

Faster than we can keep this page updated. State enforcement actions are issued, withdrawn, or expanded on regulator timelines that can shift week-to-week. The table above is current as of May 28, 2026; verify in-app before depositing. We update this page monthly, but a definitive answer requires checking the platform’s own state-availability disclosures at the time of your deposit.

Are Kalshi and Polymarket winnings legal income?

Yes — and they’re taxable. See our companion guide on are Kalshi event contracts taxable for the Section 1256 framework, 1099 reporting, and state-tax considerations.

Final reminder on professional advice

This is not legal advice. Prediction-market regulations are in flux at both the federal and state level. Court rulings, regulatory orders, and state enforcement actions can change the picture within weeks. The state-by-state table above is accurate as of May 28, 2026 to the best of our knowledge, but it should not be used as a substitute for verifying current status in-platform and consulting an attorney licensed in your state. We do not respond to “is X legal for me?” questions in email or comments — please find counsel licensed in your jurisdiction.

Stay ahead of the markets

Subscribe to the Bellwether weekly roundup — one short email each Sunday covering what’s moving on Kalshi, Polymarket, and Robinhood Event Contracts, including the latest regulatory and state-availability changes.

One email per week · Unsubscribe anytime · We don’t share your email

Where to go next

If this guide answered the legality question and you want the deeper material, the next steps depend on what you came to figure out:

- Compare the major platforms → Kalshi vs Polymarket on fees, liquidity, and state availability

- Verify your state in depth → California, Texas, Florida, New York

- Understand Polymarket’s US-relaunch details → our Polymarket breakdown

- Get the safety framework → Is Polymarket safe in 2026?

- Get the tax framework → Are Kalshi event contracts taxable?

We may receive affiliate commissions when you sign up via links on this site. Learn more (FTC disclosure). Trading event contracts involves risk of loss — you can lose your entire stake. Nothing on this page is legal advice; consult an attorney licensed in your state for your specific situation.

By Dana Okafor · Senior Legal Correspondent, Bellwether · Last updated: May 28, 2026 — we update this page when CFTC orders change, state enforcement actions evolve, or platform-side availability shifts.

Next: How to read prediction-market prices — the beginner’s pricing guide